Cars are by far the most popular and important means of transport

The car is still by far the most important means of passenger transport. According to the latest DAT report, 77% of those surveyed consider their own car indispensable for ensuring everyday mobility. In 2021, just under 87% of total passenger transport performance was attributable to so-called motorized individual transport (MIV; predominantly passenger cars). It is true that this high share can also be explained by the COVID-19 pandemic, as some people avoided public transportation due to the risk of infection. But even before COVID-19, MIV derived a share of transport performance of more than 78% (2019). At that time, public transport reached a share of 9.8% of transport performance. This shows that public transport (especially in rural areas) would only be able to absorb a limited amount of the MIV transport performance.

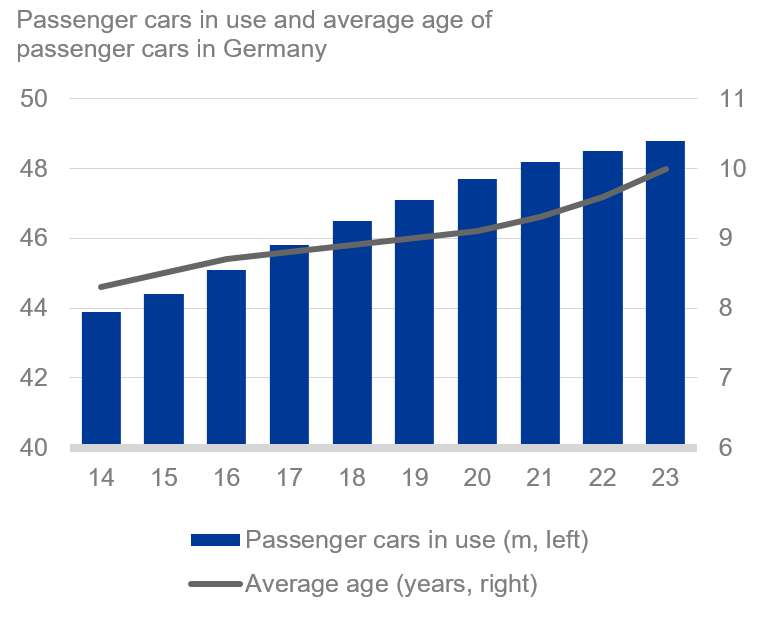

Passenger cars are getting older on average

It is not only the number of cars in Germany that is rising. At the same time, they are getting older on average. At the beginning of 2023, the average age of cars in the fleet was 10 years, according to the Federal Motor Transport Authority (KBA). This is a new record. Since 2014, the average age has increased by 2.7 years (+20.5%).

Scarce supply – higher prices

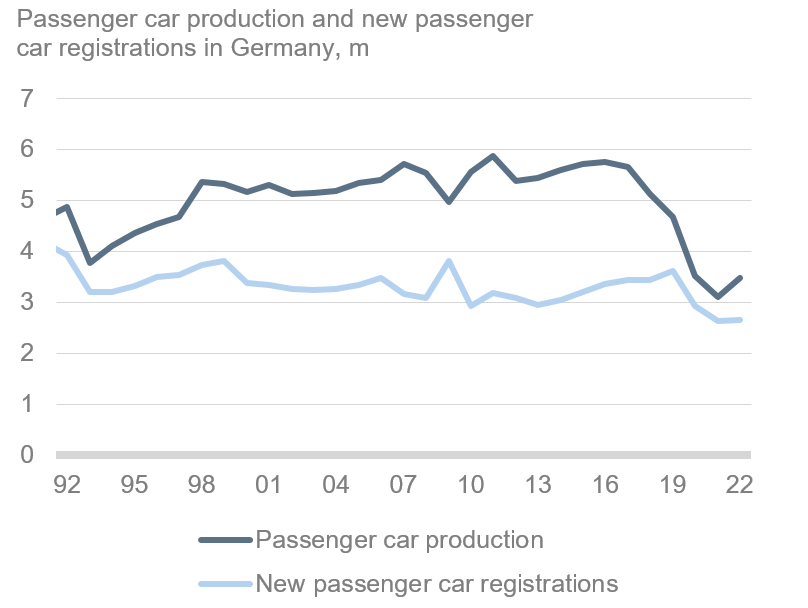

The rising average age is an extremely positive sign in terms of vehicle quality and durability. However, there are other reasons for this development. On the supply side, shortages of intermediate products (e.g. semiconductors) and other supply chain disruptions (e.g. war in Ukraine) have massively depressed production levels. From 1998 up to and including 2018, unit passenger car production in Germany (apart from 2009) was always above the 5-million-unit mark. In the years 2020 to 2022, however, an average of just under 3.4 million cars per year rolled off the production lines (low point in 2021 with 3.1 million cars). In the EU as a whole, automotive production was also affected by the shocks. With such a significant drop in supply, potential car buyers will inevitably have to wait longer for new cars and use their existing vehicles for longer.

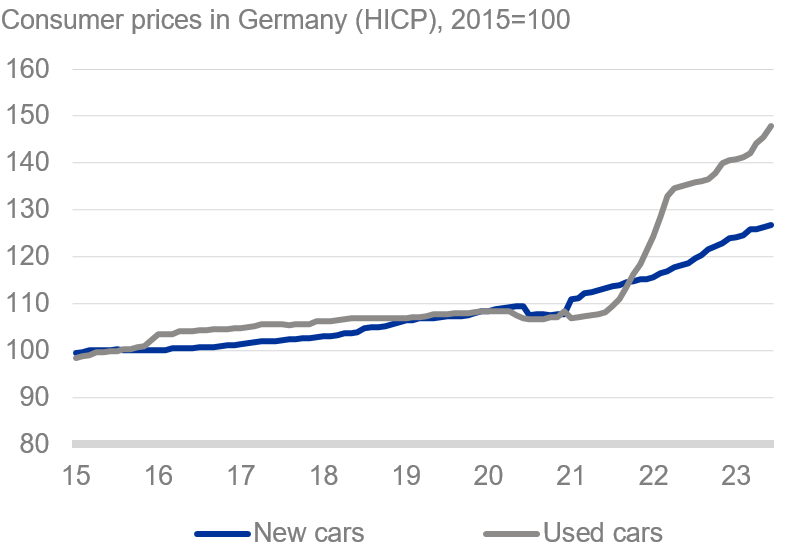

The tight supply in recent years is also reflected in the prices of new and used cars. In the first half of 2023, prices for new cars were just under 16% higher than the average level in 2020, according to the German Federal Statistical Office. For used cars, the figure was as high as 33.5%, because here too the fall in car production was indirectly causing shortages. As a result, car ownership registrations fell by 15.8% to 5.6 million in 2022, a new low in reunified Germany.

The rise in car prices is also substantial in absolute terms: according to the DAT report, the average price for new passenger cars rose from EUR 27,030 to EUR 42,790 (+58%) between 2013 and 2022. For used cars, the average price in 2013 was EUR 9,420, but last year it was already EUR 18,800 (+100%). In 2019, 44% of all used cars traded were still in the price segment up to EUR 10,000. In 2022, it was only 23%.

High prices, rising interest rates and uncertainty dampen demand

Given the price trends and supply shortages outlined above, it is hardly surprising that car demand has been subdued. Higher purchase prices have been compounded by rising interest rates for several quarters. Private households are also affected in their consumption decisions by higher energy costs and general economic uncertainty, which has a negative impact on the propensity to buy. This is reflected in new car registrations in Germany, which in 2022 were up just 1%, barely recovering from the two declines in 2020 (-19%) and 2021 (-10%). If fewer new cars are registered, this favors a rising average age in the stock. Nevertheless, new car registrations increased in H1 2023 (+13% yoy).

Costs/prices expected to continue to rise

Regulatory conditions are likely to lead to further price increases for cars with internal combustion engines in the coming years. The Euro 7 emission standards planned for 2025 will increase production costs per car. According to a study by Frontier Economics commissioned by the European Automobile Manufacturers’ Association ACEA, the additional production costs are around EUR 2,000 for passenger cars (higher cost premium for diesel cars, lower for gasoline cars). These figures exceed the EU Commission’s calculations by a factor of 4 to 10. In the volume segment, the relative cost premium per vehicle is likely to be particularly significant. In the end, drivers will have to pay the price for cleaner cars. On the cost side, there are also the announced increases in the CO2 tax in Germany, which will make gasoline and diesel more expensive.

Limited supply due to trend toward electromobility

Supply has not shrunk solely due to supply chain disruptions and other external shocks. The supply of internal combustion engine vehicles is also gradually declining with the trend toward electromobility. Some internal combustion vehicles have been removed from ranges or no longer offered in the desired engine version. At the same time, for many drivers the switch to electric cars is not yet feasible in practice because the charging infrastructure is perceived as insufficient, the charging times are too long, the range is too short, the individual requirements for one’s own passenger car cannot be met by an electric vehicle, or the price is simply too high. According to the DAT report, the range, the high purchase price and the charging time are the main reasons against buying an electric car. In this respect, the potential supply is reduced even further for some potential car buyers, which is why the existing car is used for longer. Replacement decisions might also be postponed in part because consumers hope that these problems will be reduced in the foreseeable future.

Structural entrenchment of shortages in the volume segment?

The shortage in car supply could become structurally entrenched in the volume segment or low-priced used cars in the coming years. As returns per vehicle are generally more lucrative in the premium segment, manufacturers could withdraw from the volume segment, at least in part. In our 2021 report on “Germany’s future as a carmaking location”, we had already stated that the production of “everyman cars” in high-wage countries may come under pressure. As a result, it may be difficult for low-income households to find affordable used cars in the future. The current vehicle would be driven longer, and the supply of used cars would thus be further limited. Given the high importance of the car for people’s everyday lives and because of the limited performance of alternatives in passenger transport (especially in rural areas), an economic and social policy perspective increasingly assumes that the car should not become (even more) of a luxury good. It remains to be seen how the volume segment could be served in the future, with some discussions suggesting that imports from countries with lower production costs are an option.

- Due to a change in the methodology used by the KBA to calculate the average age of vehicles, the data differs from earlier KBA publications. The average age data shown in chart 1 is based on the new methodology.

Deutsche Bank AG

Please visit the firm link to site