Recently, a discovery of so-called rare earths in Kiruna, Sweden, caused a great uproar in the media. Rare earths are a group of 17 elements that are often grouped together because they occur commonly and have similar properties. The EU Commission lists them as critical raw materials alongside metals like cobalt, lithium, and titanium. This means that they are of crucial economic importance, but cannot be reliably mined in the EU. The finding, presented just in time for the start of the Swedish EU Presidency, is therefore good news. Given the planned energy transition, the demand for critical minerals will increase rapidly, as they are needed for diverse technologies and infrastructures such as wind turbines and electricity grids. In a new report, the International Energy Agency (IEA) emphasizes that mining capacity needs to be expanded quickly to meet the net-zero targets.

High demand – critical origin

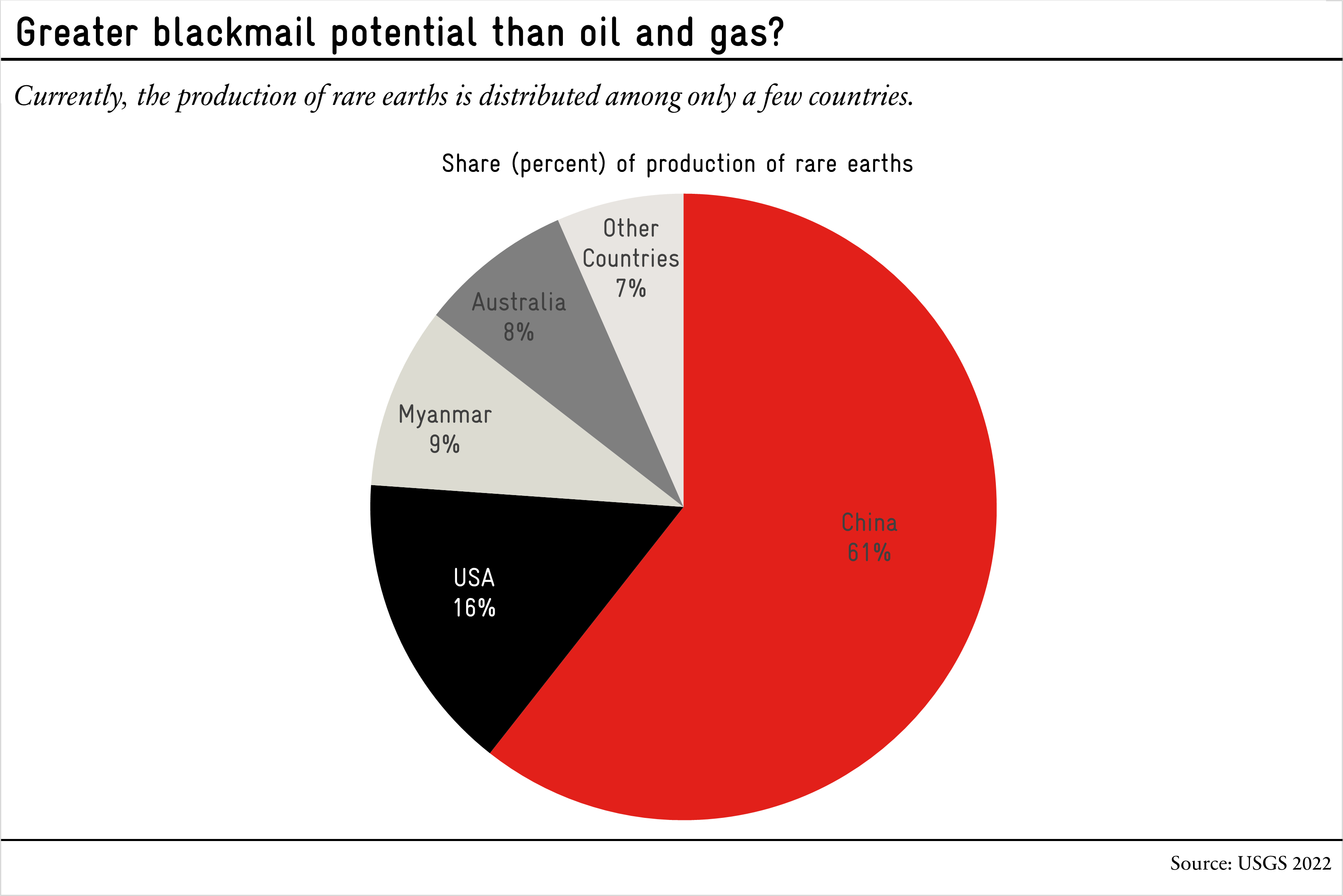

While the blackmail potential of oil and gas is gradually decreasing, the geopolitical importance of critical minerals is likely to grow. Their production highly concentrated. When it comes to rare earths, for instance, China is responsible for about 60 percent of supplies. In the case of lithium, where the IEA predicts the greatest scarcity in the coming years, Australia accounts for 55 percent of production and Chile 25 percent.

Refining is also highly concentrated. China is responsible for 90 percent of rare earth refining. For lithium and cobalt, the figure is 60–70 percent.

Large economies such as the EU and the USA have long since responded in the race for the coveted metals because, after all, they also hope for growth and jobs from the green transition. The measures they have taken are embedded in numerous industrial policies closely linked to policy on climate and energy security. For example, the EU is expected to present the Critical Raw Materials Act in March. The main thrust: In addition to expanding domestic production (20–30 percent), Brussels wants to build up a network of reliable suppliers. In the US, the Infrastructure Investment and Jobs Act also provides funding for the mining of critical minerals, such as pilot processing projects and research activities.

And Switzerland?

According to a report by the Federal Council, Swiss companies tend to be at the end of the supply chain when it comes to critical minerals. The most important condition for Switzerland’s access to critical minerals therefore remains a functioning multilateral trading system. WTO law prohibits quantitative export restrictions. For diversification purposes, Switzerland should also continue to cultivate its bilateral relations with commodity-rich states via economic diplomacy, because only through the largest possible network of trading partners can international shocks be cushioned and cluster risks avoided. However, Switzerland should avoid entering the subsidy race, as such a race cannot be won. On the contrary, foreign subsidies could make imports cheaper for this country.

The deposits found in Sweden are estimated at over one million tons. By way of comparison, China is sitting on reserves of 44 million metric tons of rare earths. The development of further sites is essential for the energy transition.

“Avenir Suisse is an independent think tank that works for the future of Switzerland by developing evidence-based, liberal, free-market ideas.”

Please visit the firm link to site