22 May 2024

Why do central banks mostly give their guidance for future monetary policy in qualitative terms rather than providing a numerical formula? The ECB Blog takes a look through the lens of the “ABCs” of the ECB’s qualitative reaction function.

For thousands of years scholars have been chasing the idea of a “theory of everything” or “world formula” – or, in the words of Goethe’s Faust: “Dass ich erkenne, was die Welt im Innersten zusammenhält” [“So that I may perceive whatever holds the world together in its inmost folds”]. Economists are no exception, even if what they study is not the universe but, more mundanely, the explanation of economic phenomena – such as inflation. Monetary economists ask questions like “is there a magic formula that delivers price stability under any circumstance?” And they speak of “monetary policy rule” rather than “magic formula” when talking among themselves.

Of course, there has been progress, building on the much-acclaimed Taylor rule published some thirty years ago which offers an elegant summary description of the relation between growth, inflation and interest rates. But the quest for a single, perfect rule has proven elusive so far. Accordingly, central banks around the world have stayed clear of embracing any particular rule. At the same time, for monetary policy to be effective, central banks need to provide to the public at least qualitative information on what guides their decisions – their “reaction function” in economic parlance. This blog post takes a look at the three elements – the “ABCs” – of the ECB’s reaction function as communicated prominently since March 2023: the inflation outlook (A), the dynamics of underlying inflation (B) and the strength of monetary policy transmission (C).

“A” – the inflation outlook

There is universal agreement in the profession that monetary policy has to be forward-looking. Monetary policy affects the economy and inflation with considerable lags. This is why the notion of inflation outlook takes centre stage in policymaking, broadly in line with the recommendations of the literature on inflation forecast targeting. At the risk of oversimplifying, these say that central banks should set their policy rates such that projected inflation converges to the target by the end of the forecast horizon, which is typically about two to three years. If, however, the forecast has inflation above (or below) target at the end of the horizon, then rates have to be set higher (or lower) than the rate path embedded in the forecast.

There are, however, obstacles to following even this simple playbook. Inflation forecast targeting was developed during the so-called Great Moderation period from the mid-1980s to 2007. Since then, the economy has been much more volatile. Two supposedly once-in-a-generation shocks actually happened within just one generation (the 2008 global financial crisis and the 2020 pandemic). These shocks put into question the reliability of historical relationships, economic models and forecasts. This is a problem for decision-makers having to act under exceptionally high uncertainty. In periods when it is extremely difficult to discern how the economy might evolve, decision-makers will naturally put less weight on forecasts of inflation in the more distant future. The reason is simple: the uncertainty surrounding the forecasts grows as the horizon lengthens. All this suggests that the horizon of monetary policy has to be context-specific, as explicitly recognised in the ECB’s monetary policy strategy statement.

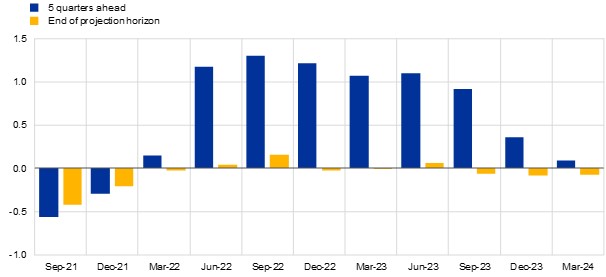

Chart 1

Deviation of projected inflation from the 2% target

Percentage points

Sources: ECB/Eurosystem staff macroeconomic projections and ECB staff calculations. Notes: For each projection vintage between September 2021 and March 2024, the chart shows the gap between projected year-on-year inflation and the ECB’s 2% inflation target for two alternative horizons. For example, for the September 2021 vintage, five-quarters-ahead inflation is the projection for Q4/2022 and end-of-projection-horizon inflation is the projection for Q4/2023.

In exceptionally uncertain times, such as those facing the euro area since 2020, the inflation outlook cannot be summarised in one number. The starting point – where is inflation today? – matters, as does the journey back to target – what is the path of inflation at different points of the forecast horizon? Chart 1 illustrates the stark difference between distance to target halfway through the projection horizon as compared to the end of the horizon for the period between June 2022 – shortly before the first ECB rate hike – and September 2023 – the latest rate hike. This does not mean that the five-quarter-ahead horizon is what drives policy. But quite naturally, in the face of exceptional uncertainty and repeated one-sided forecast errors, a forecast seeing return to target as a distant prospect does not offer much comfort to policymakers. This is even more unsettling when the current inflation rate is far from target. The chart also shows that the gap between the midpoint and endpoint of the forecast has significantly narrowed over the last two rounds, increasing the confidence in a timely return to target.

Much has been written about the forecast errors made by the ECB and central banks in general. The ECB has been transparent about those errors (see this Economic Bulletin box for latest evidence). Large forecast errors are a headache for decision-makers. Over time repeated large errors may put into question the credibility of the central bank, thereby undermining the solid anchoring of inflation expectations (discussed below). But they also offer an opportunity to learn how the economy adapts to unprecedented shocks like the pandemic. Moreover, in awareness of the limitations of point forecasts, staff have since the beginning of the pandemic supplied decision-makers with a wealth of alternative scenarios and sensitivity analyses (regularly published as part of the projection reports). Most recently, forecast errors have become smaller and risks to the inflation outlook more balanced, increasing the confidence in the projections.

“B” – the dynamics of underlying inflation

While projections are the key input into decision-making in normal times, other indicators gain in importance in uncertain times, in particular underlying inflation. Since March 2023 the Governing Council has stressed the dynamics of underlying inflation as one key element of its reaction function. But underlying inflation was also prominent in ECB communication in the past, such as the period of very low inflation before the pandemic (see this Economic Bulletin box for details) and the recalibration of forward guidance in July 2021.

The idea behind underlying inflation is to extract from today’s inflation the component that is persistent and thereby provides valuable information on inflation developments over the medium term (see this speech by ECB Chief Economist Philip Lane for a detailed discussion). Some measures of underlying inflation – such as “core inflation” excluding food and energy – are observable, but many need to be estimated.

ECB staff regularly evaluates the predictive power of a wide range of alternative measures (see this Economic Bulletin box for latest evidence). To keep it simple for expositional purposes, this blog post focuses on four measures: one that is prominent in the public debate (core inflation) and three with particularly good predictive power. Despite what its name suggests, core inflation is not a particularly good predictor of headline inflation. Both the estimated persistent and common component of inflation (PCCI) – including or excluding energy – and domestic inflation – excluding items with high import intensity – have instead performed well over a long sample.

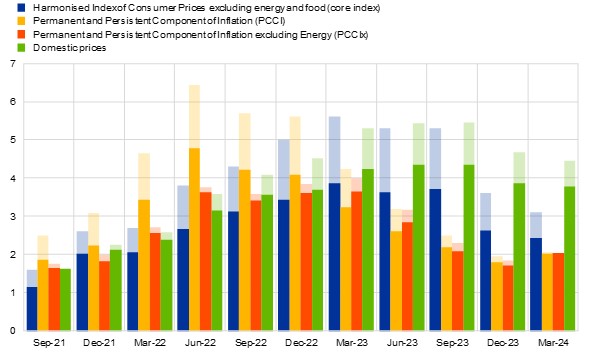

Chart 2 shows how these four measures of underlying inflation have evolved since the second half of 2021. The shaded areas in the chart also show an important recent methodological innovation by ECB staff, which was to purge the impact of supply bottlenecks and energy-related shocks on the measurements. While all measures are past their peak, a sizeable gap has opened up between the PCCI measures on one side and domestic inflation on the other. The PCCI measures have been close to 2% since last autumn, signalling that the return of inflation to target is on track. Domestic inflation, however, instead signals persistent inflationary pressures, possibly because it is closely related to wage-sensitive activities. The gap between the PCCI measures and domestic inflation is currently exceptionally large. Future data will determine which indicator will have performed best in the current episode. In any case, the dynamics of underlying inflation deserve close monitoring, in accordance with the Governing Council’s emphasis on data dependence.

Chart 2

Alternative measures of underlying inflation

Annual percentage change, publication time of new projections

Sources: ECB staff calculations. Notes: For each projection vintage between September 2021 and March 2024, the chart shows the estimated value of the respective measure of underlying inflation in the month preceding the respective projection vintage, for example the August 2021 estimates for the September 2021 projection vintage. The solid bars show the respective measure adjusted for supply bottleneck and energy shocks, while the shaded bars show the impact of those shocks on the unadjusted measure of underlying inflation. The adjustment is based on the methodology described in M. Banbura, E. Bobeica and C. Martinez Hernandez, “What drives core inflation? The role of supply shocks”, ECB Working Paper 2875.

“C” – the strength of monetary policy transmission

The third element of the reaction function may come as a surprise. Aren’t central banks supposed to know perfectly how their actions affect financing conditions, the economy and ultimately inflation? The truth is that the transmission of monetary policy itself is surrounded by uncertainty. This uncertainty is explicitly recognised in the ECB’s monetary policy strategy statement. The reason is that evolving economic and financial structures, the stage of the monetary policy cycle and the shocks hitting the economy may all affect policy transmission, either amplifying or attenuating policy impulses.

For example, at the start of the current tightening cycle it was not self-evident that the increases in the key policy rates would transmit forcefully along the yield curve and to broader financing conditions. First, while the key policy rates are the primary instrument of monetary policy, those rates had been close to the lower bound for an extended period of time. During that period the spotlight was on other instruments, such as asset purchases and longer-term refinancing operations. Second, the current tightening cycle is unprecedented in that it has taken place in an environment of very ample excess liquidity. Third, the scale and pace of policy rate hikes was unprecedented over the period since the introduction of the euro in 1999. A question mark thus hung over the potential impact of rate policy.

Almost two years into the hiking cycle, there is a wealth of evidence indicating that monetary policy transmission has been forceful (see the recent speech by ECB Chief Economist Philip Lane for a comprehensive review of this evidence and his recent blog post for a review of the ECB’s rate hiking cycle). In the euro area, with its bank-based financial system, bank credit standards and bank lending are of particular importance for transmission.

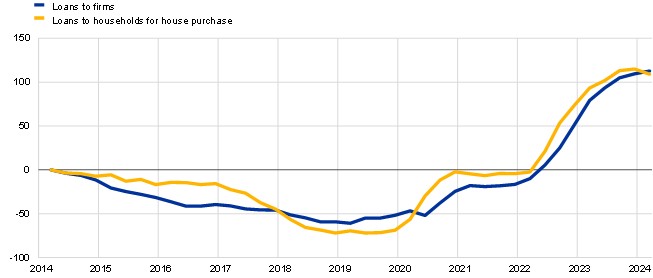

Chart 3 shows the evolution of bank credit standards over the last ten years, capturing both the period of credit easing in the low-inflation environment and the most recent period of credit tightening. Importantly, despite ample excess liquidity, euro area banks have substantially tightened their credit standards over the last two years. This has translated into a sharp decrease in loan growth, which has by and large been flat since late autumn 2022. The cumulative tightening of credit standards appears to have reached its peak for housing loans at the turn of the year and the peak seems close also for loans to firms. It is likely that banks will at some point start to gradually ease their credit standards. Yet, in cumulative terms credit standards will remain tight for quite some time and this will exert continued downward pressure on inflation.

Chart 3

Evolution of bank credit standards

Cumulated net percentages of banks reporting a tightening of credit standards

Sources: ECB Bank Lending Survey and ECB staff calculations. Notes: Net percentages for credit standards are defined as the difference between the sum of the percentages of banks responding “tightened considerably” and “tightened somewhat” and the sum of the percentages of banks responding “eased somewhat” and “eased considerably”. Cumulation starts in the first quarter of 2014. For further details see the dedicated webpage “Euro area bank lending survey” as well as P. Köhler-Ulbrich, M. Dimou, L. Ferrante and C. Parle, “Happy anniversary, BLS – 20 years of the euro area bank lending survey”, ECB Economic Bulletin, Issue 7/2023.

Hidden “D” – the anchoring of long-term inflation expectations

Inflation expectations are a key determinant of monetary policy effectiveness. Central banks are obsessed with the “anchoring” of longer-term inflation expectations. And for good reason, as the current episode makes clear when compared with experiences from the early 1970s to the mid-1980s. In that earlier period, central banks allowed inflation expectations to drift up. Bringing these down ultimately required extremely large increases in policy rates, often to double-digit levels. Monetary policy thereby had to inflict considerable pain along the way in terms of lost output and employment to bring inflation back down.

A group of time travellers starting their journey in that period and landing in today’s euro area would rub their eyes in disbelief upon hearing that policy rates peaking at 4% seemed sufficient to bring inflation back to target in a timely manner.

There are two main reasons why rates have not had to go as high as four or five decades ago.

First, the so-called natural interest rate – r* – has decreased considerably over time (see this Economic Bulletin box for latest evidence). Although estimates of r* – the real interest rate which would be neither expansionary nor contractionary – are surrounded by considerable uncertainty, there is broad agreement that r* is now lower than it was back then.

Second, and even more importantly, longer-term inflation expectations have remained close to the 2% inflation target throughout the latest episode. This reflects the credibility capital that central banks have accumulated over time. In the euro area, for example, inflation has averaged 2.1% over the euro’s first twenty-five years – a period that includes the inflation surge to about 10% in October 2022.

As long as this credibility is not put into question, longer-term inflation expectations will stay close to the target. With full credibility one will not observe any direct reaction of the central bank to longer-term inflation expectations. Of course, the ECB would react if inflation expectations started to drift away from the target. In economic parlance, a credible pledge to act forcefully is an “off-equilibrium threat”, with action only to be seen if things go horribly wrong, hence the “hidden D”. In the 1970s things indeed did go horribly wrong. Inflation expectations drifted up, driven by wage-price spirals, and central banks had to act very aggressively to realign expectations with price stability. One key lesson from that earlier period has been to put the focus on the firm anchoring of longer-term inflation expectations, with the credible pledge to act forcefully as a strong deterrent.

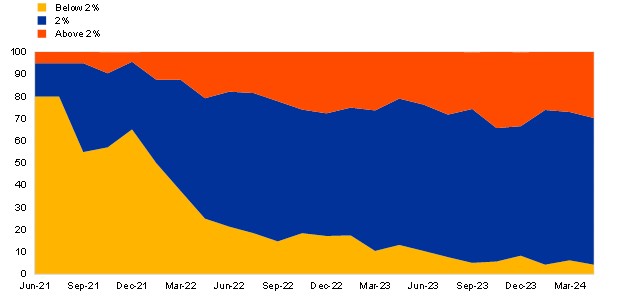

Before each policy meeting, we ask ECB watchers about their longer-term inflation expectations. Chart 4 shows the evolution of those expectations over the period since June 2021, i.e. the month before the conclusion of the ECB’s 2020-21 monetary policy strategy review. The challenge at that time was to re-anchor inflation expectations at the 2% target – from below, as witnessed by the very large yellow area. One year later, the distribution of expectations had changed considerably: centred around 2%, with roughly equal percentages of respondents with long-term expectations below and above the target, in line with the symmetry of the ECB’s inflation target. So, mission accomplished?

As discussed in this August 2022 blog post, the main challenge back then was to avoid overshooting – a de-anchoring to the upside – in the face of the ongoing inflation surge. Therefore, protecting the anchoring of expectations has required determined policy action. Another two years later, it appears that the challenge has been largely met. Most ECB watchers see inflation at 2% in the long term. At the same time, the distribution has become somewhat skewed to the upside, which requires continued alertness.

Chart 4

Evolution of long-run inflation expectations over SMA survey rounds

Percentage of respondents

Sources: ECB Survey of Monetary Analysts (SMA), all vintages from June 2021 until April 2024. Notes: The three groups are based on the long-run HICP inflation point forecasts provided by SMA respondents. The 2% bin (blue area) is calculated as the percentage of respondents with inflation expectations between 1.95% and 2.05%.

Where do we go from here? As ECB President Christine Lagarde explained in her keynote address at the recent ECB Watchers conference, the three elements of the ECB’s reaction function will remain important in the period ahead. The relative weights assigned to the elements will have to be regularly examined and, as past experience has shown, will likely change as events unfold. After all, those weights are not part of the set of “nature’s constants”.

The views expressed in each blog entry are those of the author(s) and do not necessarily represent the views of the European Central Bank and the Eurosystem.

Check out The ECB Blog and subscribe for future posts.

“The European Central Bank is the prime component of the Eurosystem and the European System of Central Banks as well as one of seven institutions of the European Union. It is one of the world’s most important central banks.”

Please visit the firm link to site