On 1 January 1909, around half a million elderly people queued up at post offices around the UK, waiting to receive the very first State Pension payments.

Only those older than 70 with an income of less than 12 shillings a week were eligible. Those who qualified received a payment of five shillings, yet the payments could be stopped if you had too much furniture in your home or were deemed to be a drunkard or “of bad character”.

The State Pension has changed considerably since then, but it’s always remained an important part of the country’s safety net, providing a regular income for retirees. Yet, many people who claim the State Pension don’t receive the full amount.

Indeed, in August 2023, FTAdviser reported that only half of the people claiming the new State Pension were paid the full amount. This may be because they have gaps in their National Insurance (NI) record and so are not entitled to the full payment.

Fortunately, the government normally allows you to top up your NI record for the past six years if you need to, so you may be able to benefit from a larger State Pension when you retire. Until 5 April 2025, you can also top up contributions for years as far back as 2006.

The recent launch of a new online tool makes purchasing NI contributions (NICs) easier than ever, but you may wonder whether you need to do this.

Read on to learn more about the new State Pension online top-up service and whether you should purchase extra years.

You need 35 “qualifying years” to receive the full new State Pension payment

The full new State Pension payment is £221.20 a week in the 2024/25 tax year. This is a significant sum and, while you will likely have private or workplace pensions to help fund your lifestyle in retirement, the State Pension can be a valuable supplement to your other savings.

Additionally, you receive the payments for the rest of your life and the amount normally increases each year by the higher of:

- The rate of inflation

- Average wage growth in the past year

- 2.5%.

As such, it’s important that you don’t overlook the State Pension when planning for retirement. However, you only receive the full amount if you have 35 “qualifying years” of NICs before you retire.

A qualifying year is any year in which you:

- Worked and paid NICs

- Paid voluntary NICs

- Received NI credits due to illness, caring for a child under 12 or a vulnerable adult, or unemployment.

If you have fewer than 10 qualifying years, you won’t receive any new State Pension payments at all and if you have more than 10 but fewer than 35, you will receive reduced payments.

There are several reasons why you might not have enough qualifying years. For example, you may have:

- Taken a career break to care for children or travel

- Returned to full-time education

- Worked abroad for a period.

You may want to check your NI record to see if there are any gaps. Luckily, if there are missing years, you still have time to top up your NICs and potentially qualify for the full new State Pension.

You can currently fill gaps in your NI record all the way back to 2006 but the deadline is 5 April 2025

The government recognises that people may have gaps in their NI record for several reasons, so they allow you to make voluntary contributions and fill those gaps.

Normally, you can make contributions for the past six years. However, when the government introduced the new State Pension on 6 April 2016, they put a transitional arrangement in place. This allows you to make voluntary NICs for years all the way back to 2006.

The deadline for this new arrangement was originally 5 April 2023, after which you’d only be able to fill gaps for the previous six years. The government then extended the deadline to 31 July 2023 and more recently until 5 April 2025.

Consequently, you still have the opportunity to correct your NI record all the way back to 2006.

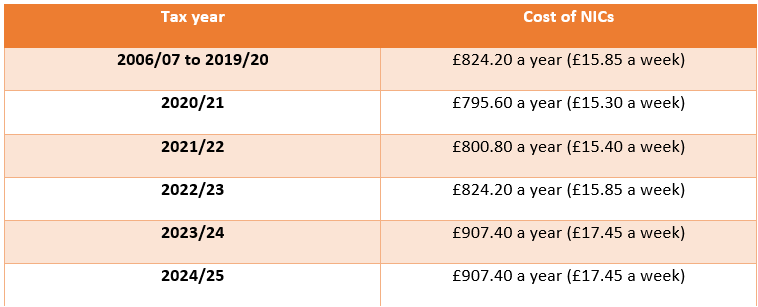

The cost of voluntary NICs varies depending on the year for which you’re paying. The following table shows how much it could cost you:

Source: Pension Bee

Previously, you had to call HMRC and make payments over the phone if you wanted to top up your NI record. However, the UK government recently launched a new online tool that allows you to check your State Pension entitlement, identify any gaps in your record, and make payments to fill those gaps.

As a result, it’s far easier to make sure that you have enough qualifying years to receive the full new State Pension payment. Yet, you might be wondering if topping up is worthwhile.

Topping up your NICs for 2022/23 could make you £2,750 better off over 10 years

When deciding whether you should fill gaps in your NI record or not, you may need to consider what it would cost and how much your new State Pension payments will increase as a result.

Additionally, consider how old you are and whether you’ll have the opportunity to reach your 35 qualifying years without making voluntary contributions.

For example, if you’re only in your 40s, you might have another 20 or 25 years at work before you retire. Consequently, you will likely exceed 35 qualifying years, so paying to fill gaps in previous years might not be worth it.

Yet, if you’re approaching retirement age, filling gaps may be more beneficial. In this case, you might want to consider the cost versus the gain, and how long you are likely to claim the State Pension for.

According to Standard Life, purchasing a full year’s worth of NICs for the 2022/23 tax year could increase your State Pension by £275.08 a year. Considering it costs £824.20 to pay NICs for that year, you would roughly break even in the third year.

So, provided you survive for more than three years, filling the gap in your NI record would create a net gain. If you claimed the new State Pension for 10 years, the single payment of £824.20 would make you at least £2,750.80 better off. Bear in mind that the State Pension amount rises each year, so the gains could be greater.

As such, it could be worth using the new online tool to check your State Pension entitlement and potentially fill any gaps in your NI record.

Get in touch

We can help you determine how the State Pension fits into your retirement plan.

Email enquiries@blackswanfp.co.uk or contact your adviser on 020 3828 8100.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available. Past performance is not a reliable indicator of future performance.

The tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

Workplace pensions are regulated by The Pension Regulator.

The post New online State Pension top-up service goes live – should you buy extra years? appeared first on Black Swan Financial Planning.

“Black Swan Financial Planning was established in 2000, and since then became one of the top independent financial adviser firms in the UK.”

Please visit the firm link to site