27 June 2024

Europe needs trillions of euros to manage climate change, become digital and defend itself. How can EU and national policymakers support these projects? This Blog post discusses the options in times of low growth and high public debt levels.

The views expressed in each blog entry are those of the author(s) and do not necessarily represent the views of the European Central Bank and the Eurosystem.

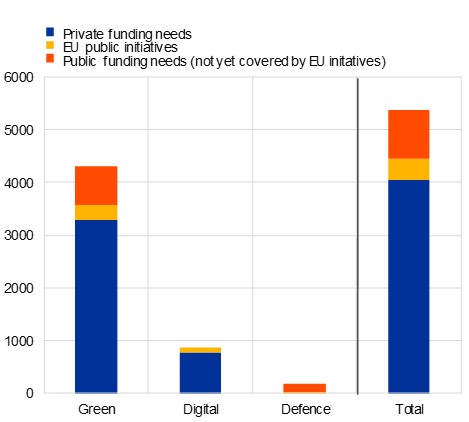

The European Union (EU) needs to move forward with the green transformation, the digitalisation of the economy and the strengthening of its military defence. This requires a lot more investment than in the past: using official estimates by the European Commission and NATO, we calculate additional €5.4 trillion for the period 2025-2031 (Figure 1)[1].

Massive investment needs…

Both private capital and governments will need to fill the financing gap. The lion’s share has to be borne by private firms, investors and households. But a substantial share – around €1.3 trillion euro, in our calculations – will have to be funded via public sources.[2]

Let’s focus on the public channel. Just under €400 billion can be expected to come from existing EU resources.[3] So, we are talking about a gap between available and needed public funding of more than €900 billion for the whole Union in the period 2025-2031, to be financed at national and EU level. While these are rough estimates, they provide an order of magnitude of the challenges ahead. To account for the high degree of uncertainty, we apply a range of +/- 20%. On this basis, the public funding gap would correspond to between 0.6% and 1% of EU GDP per year.

Figure 1

Additional cumulated EU private and public investment needs and its funding: Estimates for green-digital transitions and defence spending

(2025-2031; by funding entities and in billions of euro)

Sources: European Commission, 2023 Strategic Foresight Report. Sustainability and people’s wellbeing at the heart of Europe’s Open Strategic Autonomy; European Defence Fund (EDF); NATO; ECB staff own calculations. Notes: For the assumptions used in this chart, see footnotes 1 to 3. The chart shows the additional investment which is the difference between total investment needs and historical averages. The funding of the cumulative additional investment needs is decomposed into what is expected to be financed by the private vs. the public sector.. Planned EU investment funding initiatives include the EU budget, the Recovery and Resilience Facility (RRF) of Next Generation EU (NGEU) until end-2026, the European Investment Bank and other EU funds, as defined in footnote 3.

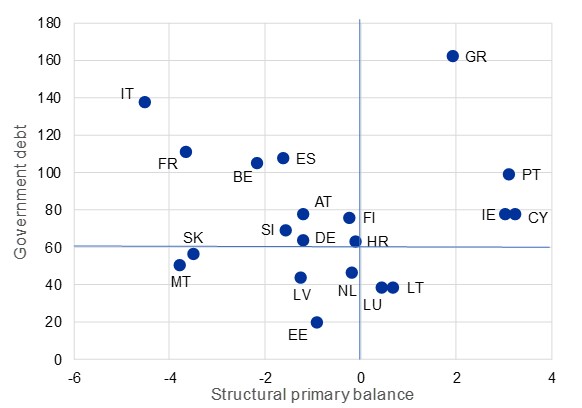

Footing this bill will not be easy, especially for high-debt countries with large structural deficits.[4] This is illustrated in Figure 2, which focuses on the euro area where countries’ fiscal positions vary considerably. Government debt-to-GDP ratios ranged between 20% and 160% in 2023. On top of that, some of the high-debt countries suffer from large underlying fiscal deficits, captured in our chart by their government budget balances net of interest expenditure and adjusted for the business cycle (“structural primary balances”).

Figure 2

Government debt ratios and structural primary balances in the euro area countries (2023)

(in percent of GDP, percent of GNI* for IE and percent of GNI for LU)

Sources: European Commission, European Economic Forecast, Spring 2024, ECB calculations Note: The horizontal line identifies the threshold – 60% of GDP – set in the EU fiscal governance to identify countries with high deficits. Ratios for Ireland and Luxembourg are expressed in percentage of GNI* and percentage of GNI respectively, which are considered better proxies of underlying economic activity in these countries.

Some help to the national governments comes from the new EU fiscal governance[5] adopted at the end of April this year, which lays more emphasis than in the past on combining fiscal consolidation needs with growth-enhancing investments and reforms. Compared with the previous governance, this may ease part of the national funding pressure for strategic investments. Two new rules may prove helpful:

First, during the budgetary adjustment phase that will start in 2025, the European Commission will give member states the option to take more time – up to seven years until 2031 – to implement their fiscal consolidation plans and put their debt trajectories on plausibly declining paths. This implies that governments would have to meet lower fiscal adjustment requirements each year. But it would be allowed only if the Commission finds that countries are implementing credible investment and reform plans. We estimate that this novel framework may create fiscal space for public investment in the EU for up to €700 billion over the period 2025-2031[6].

Second, once the fiscal adjustment phase is over, member states are allowed to keep structural public deficits at 1.5% of GDP, which are higher than in the past[7]. This would in principle give up to one percentage point more fiscal space for investment than under the previous rules.

This breathing space helps, but will it be enough?

There are reasons to believe that it may not be the case. The additional investment will foster potential growth, and therefore mitigate the risks to debt sustainability,[8] but only with a time lag. Implementation bottlenecks will emerge, such as limited administrative capacity in the public sector. Also, the estimates of the investment needs presented above are rather conservative; they do not consider other strategic investment required in areas such as health or education. For some countries, the fiscal space made available by the new fiscal rules may still not be sufficient. And even the countries which start from a comfortable fiscal position and can afford spending more than others should be concerned. No country, not even the richest, can stop climate change on its own. Strategic investments pursue shared goals and, as such, they also require common responses[9].

…call for a coordinated approach in Europe

Our back-of-the-envelope calculations lay bare the tension between investment needs and fiscal space that Europe’s policymakers are facing.

There is no silver bullet one can count on. More investment-friendly EU fiscal rules go in the right direction, but disproportionate reliance on public investment at national level would not only encounter limits in terms of administrative capacity and risk crowding out private investment; it would also not be affordable from a public finance perspective. As Figure 1 suggests, the bulk of funding of strategic investment will need to come from private sources, and even this will not be enough if not supported and integrated by EU-level initiatives.

This calls for a coordinated, holistic, and multi-pronged approach to both private and public investment in Europe, involving a wide range of initiatives at both the Union and the national level. Without claiming to be exhaustive, in Figure 3 we provide examples of complementary policy avenues – some already existing but in need of being enhanced, others more innovative.

These initiatives would reinforce each other.

To mobilise private funding, a fully-fledged European capital market would need to be accompanied by a strengthened single market, better framework conditions for doing business, more investment-friendly corporate taxation, as well as more specific initiatives, such as those listed in the first column of the table.

In high-debt countries, growth and debt performances will depend on how successfully the governments implement the Recovery and Resilience Plans of Next Generation EU. Whether countries are able to comply with fiscal adjustment requirements in an investment-friendly way will be crucial here. This includes improving the quality of public finance by cutting less productive expenditure.

The public funding gap of €900 billion, however, cannot be closed without additional involvement of the Union. The next EU budget (2028-2034) could act as a catalyst by financing investment in genuine EU public goods,[10] ranging from joint procurement in defence to energy grids, from high power computers to EU cloud expansion. Budget reprioritisation, new own resources, and joint borrowing[11] are all avenues to consider.

Figure 3

Menu of options to address additional investment needs in the European Union

null

“The European Central Bank is the prime component of the Eurosystem and the European System of Central Banks as well as one of seven institutions of the European Union. It is one of the world’s most important central banks.”

Please visit the firm link to site