3 September 2024

Euro area exporters are facing tougher competition from China. But why is that? The ECB Blog looks at the important role played by price competitiveness and the ongoing industrial upgrades being made in China.

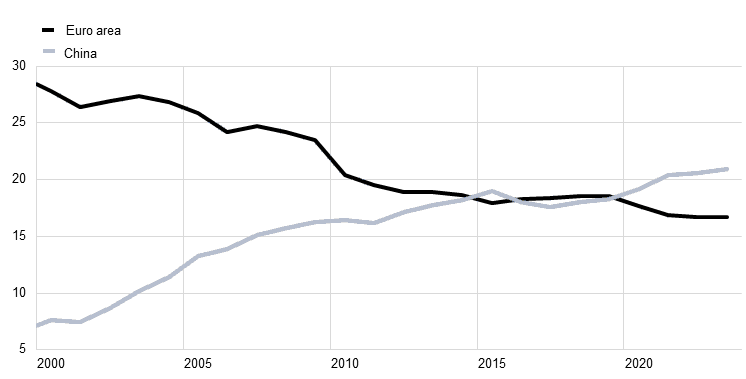

Euro area manufacturers have long benefited from Chinese exports, such as using cheap parts to produce their own finished products. In recent years, however, China has increasingly become an exporter of final goods itself. This has coincided with significant decline in the euro area’s share in the global export market, while China’s share has steadily increased (Chart 1). In this post, we look at what is behind this and what it means for euro area exporters.

Chart 1

Global non-energy goods export market shares

(percentages)

Source: Trade Data Monitor

Notes: Market shares in values of manufacturing exports excluding energy and other specific and non-classified products (HS2 sectors 25, 26, 27, 97, 98, 99). The euro area export market share shows extra-euro area trade. Latest observation: 2023.

China’s export strength is of course not the only reason for the euro area’s declining share, which has fallen by eleven percentage points since 2000, a similar but more gradual than the decline of the share of the United States. Two additional factors play a role: Europe’s gradual transition from a manufacturing-based to a more services-oriented economy and the rising integration of China and other emerging economies into the global market drive the longer-term trend.

Additionally and more recently, global preferences shifted during the pandemic, with demand moving away from goods and markets in which the euro area has historically specialised, i.e. capital goods like machinery and electrical equipment.[1] Supply disruptions, also brought on by the pandemic, compounded these difficulties because of European exporters’ deep integration in regional and global supply chains.[2] Finally, the energy shock following Russia’s invasion of Ukraine meant higher energy and other input costs, eroding euro area exporters’ price competitiveness further.

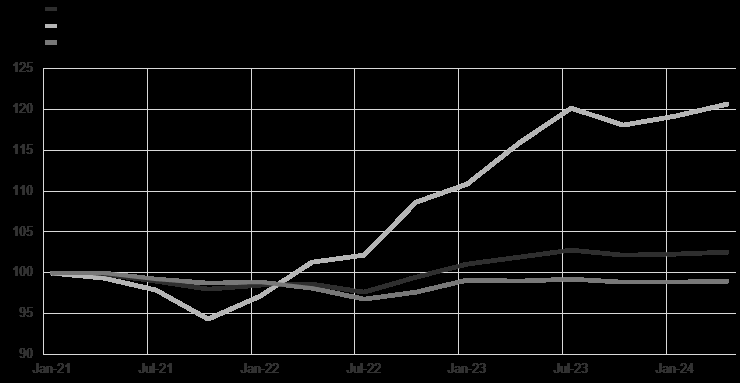

Euro area and China are now in direct competition

Our analysis indicates that recent losses in euro area price competitiveness are particularly linked to competition from China. Since 2021, China has accounted for the euro area’s entire appreciation in the real effective exchange rate based on producer prices (Chart 2). This measure lets us compare price developments vis-à-vis other countries and regions. Since the nominal CNY-EUR exchange rate remained broadly stable over this period, the euro area’s competitiveness loss is primarily due to an unfavourable evolution of the relative Producer Price Index (PPI). Simply put, euro area products became more expensive vis-à-vis Chinese products, for reasons we discuss in more detail below.

Chart 2

Euro area real exchange rates

(index, 2021Q1=100, increase=worsening price competitiveness)

Source: ECB.

Notes: China’s share in manufacturing trade is used as weight to exclude China from the real effective exchange rate. Latest observation: 2024Q2.

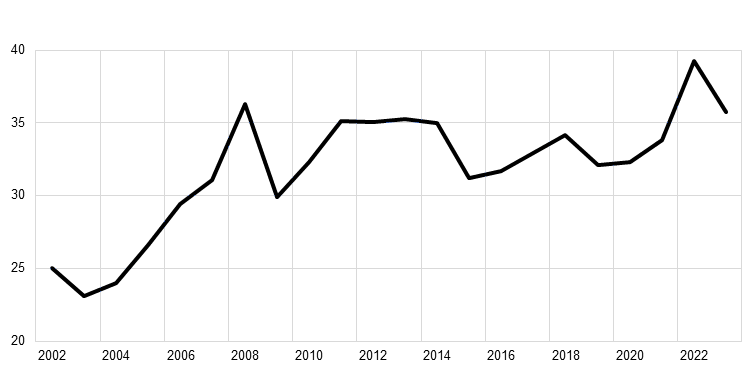

The impact of shifts in price competitiveness between the euro area and China hinges on their direct competition in export markets. While cheap intermediate products from China make input cheaper for euro area firms, they also pose a challenge if both compete with their end-products in the same markets.[3] Two decades ago, China competed mainly in low-value sectors, such as clothing, footwear, or plastic. That mostly affected southern euro area economies, which were exporting the same types of goods. As China’s exports have moved up the value chain, they are challenging more and more European exporters, including those in high value-added industries like automotive and specialised machinery. Indeed, the number of sectors in which both the euro area and China have a revealed comparative advantage (RCA) – meaning they export more in these sectors than the global average – has increased steadily in recent years (Chart 3).

Chart 3

Sectors in which the euro area and China have an RCA compared to rest of the world

(percentages)

Sources: UNCTAD and ECB staff calculations. Notes: Sectors with RCA>1 in both the euro area and China, as a share of the number of sectors in which the euro area has RCA>1. In total, 259 sectors are being considered for each year. Euro area aggregate computed as a weighted average based on export value weights. Latest observation: 2023.

With Chinese and euro area firms increasingly competing in similar export markets, price competitiveness differences matter more and more – and China gained significant price competitiveness vis-à-vis the euro area in recent years. Chinese export prices have been declining primarily because of three factors. First, the downturn in the country’s real estate market has dampened demand, resulting in substantial price reductions for certain commodities. Steel export prices, for example, have dropped by more than 50% since the start of the downturn in 2022, as have cement export prices.[4] Second, China’s advanced manufacturing sectors are gaining a significant cost advantage due to substantial government subsidies, in particular in high-tech sectors.[5] Third, excess capacity within China’s domestic market is intensifying domestic competition, leading to a decline in prices and a compression of profit margins inside the country.[6] This makes exports an increasingly important source of revenues as profit margins outside mainland China, and especially in the euro area, can be substantially higher.[7] Chinese electric vehicle makers have already assumed a dominant position in Southeast Asia despite selling at a premium relative to the domestic market. Given their comparatively higher profit margins, Chinese firms also have considerable room to further reduce their prices, thereby enhancing their competitiveness with respect to euro area firms.

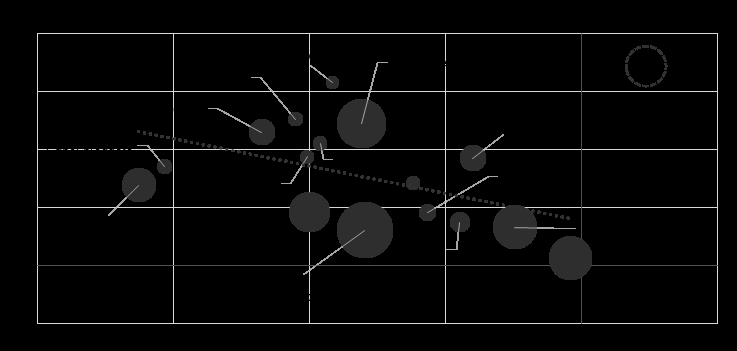

The increasing price competitiveness pressures in the last four years have already dampened euro area export performance. Indeed, export market shares fell particularly in sectors in which euro area prices increased relatively more than Chinese prices. This trend is illustrated in Chart 4, which shows euro area export market shares declining sharply in sectors where euro area producer prices have risen more than those of China particularly in high-energy intensive sectors. To understand the chart, keep in mind that the size of the bubbles represents how much each sector contributes to total euro area exports. Bigger bubbles mean the sector is more significant for euro area exports, and their position shows how much prices have changed and how market shares have shifted. For example, the car industry faced between 2019 and 2023 disadvantages in their producer prices relative to Chinese manufacturers of 7.5 percent and a loss of market share by more than 15 percent.

One major reason for this recent shift is the euro area’s struggle with the energy crisis, which has hit energy-intensive sectors like basic metals (iron and steel) and chemicals/plastic products particularly hard. These sectors have seen significant drops in both price competitiveness and market shares. Another factor is China’s excess capacity in several manufacturing sectors. In the motor vehicles sector, for example, China has gained market share from the euro area, especially in battery electric vehicles (BEVs), thanks to its dominance in global battery production and resulting price advantage.

Chart 4

China-euro area relative price changes and relative market share changes

x-axis: relative China-euro area PPI change between 2019 and 2023 (percentages), y-axis: relative China-euro area export market share change between 2019 and 2023 (percentage points)

Source: Haver, TDM and ECB staff calculations.

Notes: Export market shares in values. The sectors food and wood are excluded from the scatterplot. Size of bubbles based on share of each sector in total extra euro area exports in 2023.

Going forward, the competitive pressure from China is set to intensify significantly. Production plans for green energy technology such as BEVs entail a sharp rise in output, which is projected to significantly outpace growth of domestic demand, further compounding existing overcapacities in these sectors. China is also investing substantially in additional export shipping capacity. For instance, the scheduled delivery of additional shipping vessels is projected to significantly increase China’s annual export capacity of cars multiple times over between 2023 and 2026. The global absorption of these additional exports likely necessitates a further compression of profit margins, thereby increasing competitiveness pressures on euro area exports over the coming years.

Euro area manufacturers must adapt to this evolving landscape, not least because the sector employs over 20 million people and makes up 15 percent of euro area GDP. Embracing innovation, investing in sustainable and energy-efficient technologies, and enhancing supply chain resilience are steps that can help bolster competitiveness. Additionally, strategic market diversification and closer collaboration within the euro area could help mitigate the risks posed by the external challenges. Furthermore, policymakers should aim at developing a fair and level playing field for the trade links with China.

The views expressed in each blog entry are those of the author(s) and do not necessarily represent the views of the European Central Bank and the Eurosystem.

Check out The ECB Blog and subscribe for future posts.

For topics relating to banking supervision, why not have a look at The Supervision Blog?

“The European Central Bank is the prime component of the Eurosystem and the European System of Central Banks as well as one of seven institutions of the European Union. It is one of the world’s most important central banks.”

Please visit the firm link to site