23 September 2024

Hedge funds have substantially increased their trading activity in euro area government bond and repo markets. The ECB Blog evaluates how this plays out for market functioning and intermediation.

Government bonds are central to the broader landscape of financial markets. As high-quality liquid assets, they are an essential component in investor portfolios, and their rates serve as a benchmark for the pricing of other financial assets. The smooth functioning of government bond markets is therefore essential for maintaining a healthy and efficient market environment.

In recent years, euro area government bond (EGB) markets have witnessed a surge in the activity of hedge funds. Hedge funds are specialised investment vehicles that deploy complex strategies, including short-selling, leverage or derivatives, to improve their performance. They thrive in the context of high volatility, face fewer regulatory constraints than banks and are more flexible in adjusting their portfolios than traditional investment funds.

In this blog post, we explore the implications of this market transformation, examining how hedge funds influence the absorption and functioning of euro area bond and repo markets.

Hedge funds play an increasing role in bond market trading

The shifting macroeconomic landscape since the COVID-19 pandemic, along with significant monetary policy adjustments, has coincided with increased market volatility. Moreover, regulatory changes following the global financial crisis have imposed additional costs associated with balance sheet extensions for dealer banks, affecting their ability to intermediate in government bond markets.[2]

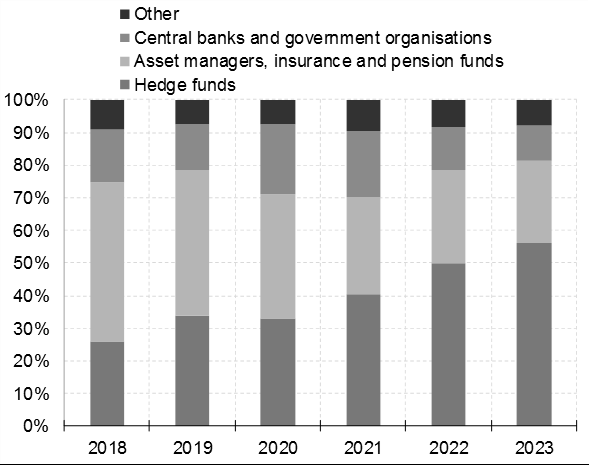

In this context, foreign investors have contributed significantly to absorbing the net supply of government bonds across the euro area, particularly since the onset of the Eurosystem’s balance sheet reduction. Among foreign investors, hedge funds have assumed a prominent role in EGB markets. Data from one leading electronic platform for the trading of bonds show that hedge funds roughly doubled their volumes of EGB transactions in secondary markets from 2018 to 2023 (Chart 1). According to this data, hedge fund activity represented 56% of volumes in the secondary market in 2023, up from 26% in 2018. This trend appears to have coincided with a migration of experienced staff from banks and asset managers to hedge funds.[3]

Chart 1

Electronic trading volumes by investor sector

(percentage share in the secondary market)

Source: Tradeweb. Notes: Tradeweb is a dealer-to-customer platform that covers a large proportion of trading in euro area government bond markets, although representativeness across time and countries may vary.

Although hedge funds may not hold government bonds for extended periods, their substantial trading volumes and their strong participation in public debt auctions indirectly support bond absorption. According to an ad-hoc survey of large primary dealers carried out by the ECB Bond Market Contact Group, hedge funds now represent over 50% of the total requests received by dealer banks around public debt auctions in Germany, France, Italy and Spain. Hedge funds thereby contribute to the success of government bond auctions both by placing orders directly with dealer banks and by facilitating the offloading of dealers’ allocations after the auction.

At the same time, the rapid increase in hedge funds’ market presence may raise concerns about whether dealer banks can sustainably intermediate the growing volumes of hedge fund activity in EGB markets. While the high trading volumes of hedge funds may help ease intermediation constraints and improve market liquidity during normal times, a sudden withdrawal of hedge funds from government bond markets could place pressure on banks and create trading bottlenecks during periods of stress.

Little evidence for amplified volatility yet

Hedge funds’ presence could be a double-edged sword for market functioning. On the one hand, hedge funds are frequently credited with enhancing market efficiency and liquidity. On the other hand, they could also act as potential amplifiers of volatility and market shocks. So, what does the evidence reveal about the relationship between hedge fund behaviour and volatility in EGB markets?

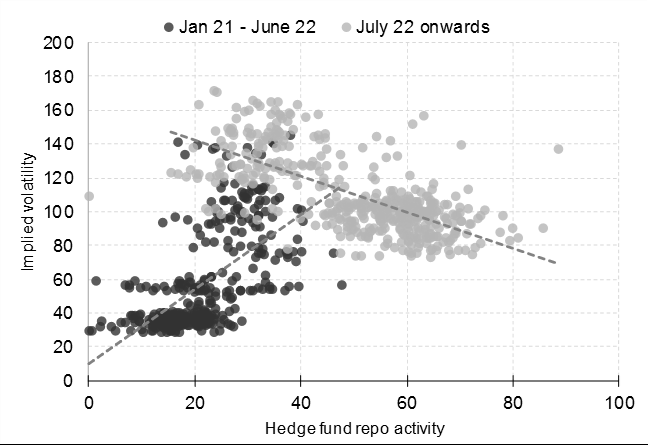

To address this question, we resort to granular data about hedge fund activity in euro area repo markets. Hedge funds often employ a strategy called short-selling, where they sell a security they do not own, betting on a decline in its price. They then fulfil the delivery of the bond by borrowing the security through the repo market. Additionally, the repo market enables hedge funds to employ higher leverage, thereby enhancing the returns of their trading strategies, such as basis trades.

The gradual increase in hedge funds’ repo market activity coincided with rising volatility in bond markets in the period before the ECB began raising interest rates in July 2022 (Chart 2). However, this correlation reversed once the rate-hiking cycle began in that month, including after the start of the gradual run-off of the asset purchase portfolio in March 2023. Thus, there is little evidence that an increased market presence of hedge funds could structurally contribute to amplified volatility dynamics.

Chart 2

Hedge fund repo volumes and bond market implied volatility

(X-axis: billions of EUR; Y-axis: index)

Sources: SFTDS, Bloomberg. Notes: Implied volatility from swaptions, SMOVE3M Index. Hedge funds repo activity is based on ESA 2010 sector S124 repo transaction volumes, either in the security lending or borrowing directions. Repo transactions against DE, FR, IT and ES government collateral for all tenors. Last observation: 29 April 2024.

However, the potential correlation between hedge fund strategies could pose challenges to the resilience of markets in times of stress. The interconnectedness of hedge fund activities, including the diffusion of pod structures[4], and their reliance on leverage means that rapid unwinding of positions – whether due to margin calls or strategic shifts – could contribute to market volatility.

Euro area banks’ exposure to hedge funds: still concentrated but gradually diversifying

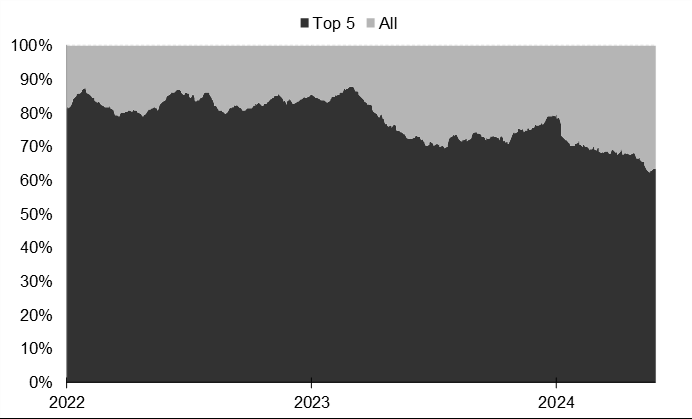

Hedge funds partly rely on banks to fund their activities. This exposes banks to risks inherent in hedge funds’ performance and strategies, for example via the repo market. Exposures there are highly concentrated among a few large players, with five euro area banks accounting for 64% of repo borrowing from hedge funds (Chart 4). This concentration poses a potential vulnerability, especially if banks were to have incomplete information about the totality of hedge funds’ positions or risks. At the same time, banks’ repo exposures to hedge funds are collateralised, which partially mitigates their risk.

Chart 3

Concentration of euro area banks’ exposure to hedge funds

(percentage)

Source: SFTDS, ECB calculations. Notes: Figure shows top 5 euro area banks’ exposure to hedge funds. Shares based on outstanding amounts of banks borrowing cash. Open repos are excluded. Last observation: 31 May 2024.

Reassuringly, the concentration of banks’ exposure to hedge funds has gradually declined over time (Chart 4), although it remains elevated. Additionally, hedge funds account for only about 10% of outstanding repo volumes[5], and banks’ exposures are diversified across approximately 200 hedge funds.

Conclusion

The increased presence of hedge funds in the euro area government bond space marks a significant recent shift within euro area financial markets. Looking ahead, hedge funds are likely to remain key players in EGB markets, backed by both substantial financial and also human capital. However, questions remain about the persistence and the reliability of hedge funds’ presence in this market segment, particularly under conditions of market stress. The scale of their activities underscores the potential amplification effects of rapid strategy reversals, which could lead to heightened volatility and pose challenges for the smooth functioning of government bond markets.

“The European Central Bank is the prime component of the Eurosystem and the European System of Central Banks as well as one of seven institutions of the European Union. It is one of the world’s most important central banks.”

Please visit the firm link to site