14 November 2024

The Eurosystem has started to reduce its bond holdings. This ECB Blog post investigates how strongly the shrinking balance sheet affects long-term interest rates. Estimates based on the Survey of Monetary Analysts suggest: an expected €1 trillion reduction in bond holdings may raise long-term risk-free interest rates by about 35 bps.

The ECB reacted forcefully in response to the recent inflation surge. The Governing Council used its primary tool of increasing key interest rates. It also initiated a pivot in its balance sheet policy, shifting from quantitative easing (QE) to quantitative tightening (QT). Under QE, beginning in 2015, the ECB and the national central banks of the euro area had purchased private and public bonds. The aim was to ease financing conditions for the economy, stimulate growth and eventually raise inflation rates and bring them back to target. Under QT, the Eurosystem has been reducing bond holdings since early 2023, when it began normalising monetary policy. How does a shrinking Eurosystem’s balance sheet affect financial conditions? For central banks worldwide, the transition from QE to QT marks relatively uncharted territory. So far, we therefore know little about how big the impact of QT on market interest rates is. The expectations of market participants, gathered in the Survey of Monetary Analysts (SMA), provide a helpful outlook.

Balance sheet shrinkage from the perspective of market analysts

We used responses from that survey, which the ECB conducts every six weeks, to gauge the impact of QT on long-term rates in the euro area.[1] In each SMA about 50 banks and asset managers provide their views on the future evolution of key monetary policy parameters, financial market variables, and the economy. We used three of the questions as the basis of our investigation: analysts’ expectations about long-term interest rates, the ECB’s policy rate, and the size of the Eurosystem’s asset purchase portfolios in the future.

Specifically, analysts tell us where they expect ten-year interest rates on overnight index swaps, as well as on sovereign bonds, to be in 12 months’ time. They also tell us where they expect policy rates to be at the end of each quarter over the following three years and in the long run. We used these three variables to calculate what we call “the one-year-ahead expected term premium”. That is the differential between two expected yields: first, what analysts expect to earn by locking in a ten-year rate in one year’s time and, second, what they expect to earn by rolling over the same investment for the same period at expected short-term rates.

In the next step, we examined how this figure interacts with the expected bond holdings on the Eurosystem balance sheet. The evidence from this exercise tells how much a given amount of balance sheet reduction is expected to increase the term premium, and hence long-term rates. We used the survey data for the period between December 2022, when QT was first announced, and December 2023.

The impact of QT on long-term interest rates

First, we found that the lower an analyst estimates the future bond holdings, the higher they expect the term premium to be. Our calculation reveals a sizeable correlation between the two. For instance, a mechanical reduction of ECB bond holdings by €1 trillion could increase the term premium embedded in the ten-year overnight index swap rate by about 35 basis points (see Chart 1). Monetary analysts therefore expect that QT will result in an increase in long-term interest rates via higher term premia.

Chart 1

Expected term premium impact from running down the asset portfolio by €1 trillion

Basis points

Sources: SMA and author calculations. Notes: The chart depicts the expected effect on the term premium of various assets with a ten-year maturity resulting from an expected €1 trillion decrease in the ECB’s bond holdings.

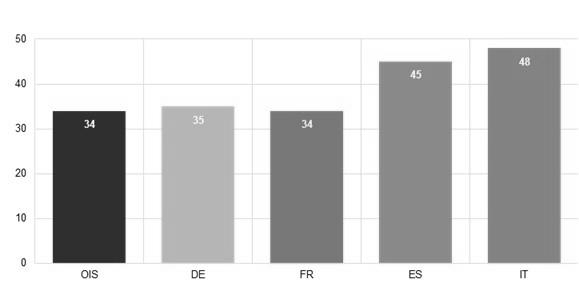

Second, we find that the prospective upward pressure of QT on borrowing costs could differ along national borders and would not be identical for all sovereign bond markets within the euro area. Specifically, a similar-sized reduction in ECB bond holdings is estimated to increase the term premium on German, French, Italian and Spanish sovereign bonds by about 35, 35, 45, and 50 basis points, respectively.[2] This means that, according to the analysts surveyed, QT would have an asymmetrical impact on financing conditions for governments across the euro area. It also means that sovereign borrowing costs could rise, and – presumably – would do so to a larger degree for countries with lower credit ratings, such as Spain and Italy.

Third, our findings suggest that the estimated impact of QT on long-term interest rates is comparable in scope to the inverse effects of QE found in previous studies.[3] Using a variety of different methodological approaches, these previous studies indicate that increasing the Eurosystem bond holdings (QE) by €1 trillion reduces ten-year rates by about 35 to 65 basis points. Thus, even if the size of QT’s effect estimated by us ranks at the lower end of the range, the comparison suggests a broadly similar impact – but in the opposite direction. That said, the estimates are subject to substantial estimation uncertainty.

Conclusion

Though the ECB’s policy interest rate has been the main instrument to fight inflation, the reduction of the Eurosystem’s balance sheet also contributes to this. Certainly, our survey-based analysis cannot measure the exact effects of quantitative tightening on financial conditions. Nevertheless, the views of monetary analysts can serve as a proxy to help understand this aspect of how our monetary policy affects financial markets and ultimately the economy. They provide us with valuable insights into how market participants perceive the ongoing balance sheet reduction and its consequences. The Survey of Monetary Analysts therefore offers relevant indications as to how big of an effect QT might have on financing conditions.

The views expressed in each blog entry are those of the authors and do not necessarily represent the views of the European Central Bank and the Eurosystem.

Check out The ECB Blog and subscribe for future posts.

For topics relating to banking supervision, why not have a look at The Supervision Blog?

“The European Central Bank is the prime component of the Eurosystem and the European System of Central Banks as well as one of seven institutions of the European Union. It is one of the world’s most important central banks.”

Please visit the firm link to site