3 December 2024

At the height of the financial crisis Greece, Ireland, Portugal and Cyprus needed help. The international assistance came under the condition of economic adjustment aiming to restore financial stability, debt sustainability and growth. How did the four countries recover from their crises?

Many euro area countries experienced fiscal troubles and financial stress during the crisis years, especially during the period from 2010 to 2012. A few even faced the risk of not being able to pay their bills – servicing their debt or paying public sector salaries and pensions – as economic conditions deteriorated, sovereign funding became more expensive and banks stumbled. In the euro area, Greece, Ireland, Portugal and Cyprus were the four countries most affected. In the run-up to the crisis, national economic policies and insufficient EU governance had allowed economic fundamentals to deteriorate. What happened? Some governments ran too high deficits, in part as fiscal rules were not implemented effectively. And they ignored rigidities in labour and product markets and an overall loss of competitiveness. The close links between banks and national governments contributed to the vulnerabilities. Ultimately, confidence evaporated that these countries would be able to prosper under the conditions of a single currency. The crises that resulted brought major economic costs and social hardship, which were rooted in the period before the programmes and continued during the difficult adjustment period that followed.

The governments of Greece, Ireland, Portugal and Cyprus asked for financial assistance and received it, the bulk of it from the euro area member states and the International Monetary Fund (IMF).[1] The loans came under the condition that the countries enact deep changes to public policies and the way their economies function, so as to restore sound economic and financial fundamentals. The EU/IMF -programmes aimed to regain fiscal and financial system stability, restore competitiveness and achieve higher and more sustainable growth while also seeking to mitigate the inevitable economic and social costs. This required fiscal consolidation and productivity-enhancing structural reforms, to get their economies back to health and “fitness”. Structural policies that support employment and real income growth can limit the need for spending cuts and tax increases and the associated social costs. Countries with an own national currency would have had the option to adjust and regain competitiveness by lowering policy interest rates and devaluing the exchange rate. As Greece, Ireland, Portugal and Cyprus are part of a currency union, the euro area, they no longer have a national currency or interest rate of their own and thus didn’t have that option Therefore, national economies had to adjust in part through so called internal devaluation, i.e. lower wage and price growth compared to the rest of the euro area, to restore competitiveness in terms of costs and prices.

This post does not assess the design of the programmes or the quality of their implementation.[2] It instead focuses on longer-term economic developments since the early 2010s. Almost 15 years later, we take stock of how well the four countries have performed since.[3]

So, how did the four countries fare?

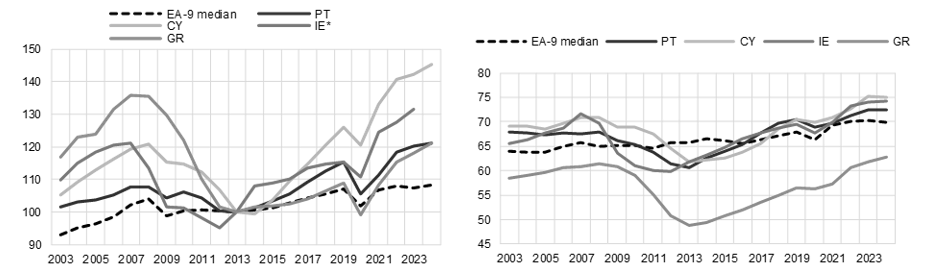

Let’s look at growth and employment first. During the crisis, all four countries went through a severe economic downturn with massive job losses, even relative to other euro area countries. The collapse in economic output (GDP, gross domestic product) began well before the programmes were agreed and implemented. And it lasted until about 2012-13. After that trough things got better. Over the last ten years all four countries recovered remarkably well, outperforming the rest of the euro area in terms of economic output and job creation (Chart 1).

However, not all of them recovered equally quickly. While for Ireland, Portugal and Cyprus, the recovery started in the period from 2012 to 2014, Greece’s upturn began later. That was because Greece faced the biggest challenges, and partly, because the sovereign debt restructuring was delayed. The political crises in 2012 and 2015 further worsened the situation. Yet, all four countries have performed strongly since 2019 and even continued to recover despite shocks such as the pandemic, the Russian war against Ukraine and the associated energy price surge.

Chart 1

Left: Real economic output per capita Right: Employment rate

(left: 2013=100; right: percentages)

Sources: Ameco, LFS, Central Statistics Office Ireland, and authors’ calculations. Notes: EA-9 refers to the following nine countries: Germany, France, Italy, Spain, Austria, Finland, Luxembourg, the Netherlands, and Belgium, i.e. the countries which have joined the euro from the beginning in 1999, excluding Ireland and Portugal. Left: For Ireland the modified gross national income (GNI*) is used (available until 2023) since GDP is distorted by specific transactions of multinational enterprises, which are in part associated with tax optimisation strategies. Figures for 2024 include forecasted data. Right: The year 2024 only covers the first two quarters of the year.

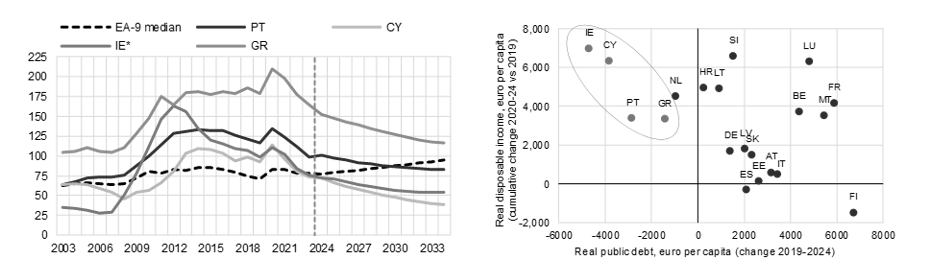

Second, how about government debt? During the crisis, government debt had soared and reached more than 100% of GDP in all programme countries in 2013. However, except for Greece, debt levels started declining after the crisis, only interrupted by the major pandemic shock in 2020. Since then, the government budgets in all four countries have improved. Cyprus, Ireland and Portugal even recorded budget surpluses in 2023.

This trend is expected to continue. The European Commission projects that public debt-to-GDP ratios will steadily decline over the next ten years in all four countries. This is a clear contrast to the EA-9[4] countries (Chart 2 left) and helps Greece, Ireland, Portugal and Cyprus to become more solid debtors in the eyes of investors. This pays off: although the four still have to pay a higher interest than fiscally stronger euro area countries, risk premia have decreased. Their longer-term sovereign yields fell below those of Italian public bonds, with Irish, Portuguese and Cypriot now even below French yields. In all four countries real public debt per capita is now lower than in 2019, while increases in real disposable income during this period have been stronger than in many other euro area countries (Chart 2 right).

Chart 2

Left: Government debt to GDP ratioRight: Change of government debt per capita and cumulative change of real disposable income per capita

(left: % of GDP, % of GNI* for IE*; right: euro per capita)

Sources: European Commission’s Debt Sustainability Monitor (DSM) 2023, Ameco, Eurostat, Central Statistics Office Ireland, and authors’ calculations. Notes: Left: Data from Ameco and Central Statistics Office Ireland used until 2023, and DSM 2023 monitor for the posterior forecast years. The DSM 2023 was based on the European Commission’s autumn economic forecast and as such does not yet incorporate final government debt figures for 2023. For Ireland the GNI* is used as denominator. Because GNI* for IE is only available until 2023 and the European Commission’s outlook for government debt is only available as a percentage of GDP, we approximate GNI* growth for IE from 2024 onwards with nominal GDP growth. Right: The values on the x-axis show the change in real public debt per capita in euro from 2019 to 2024. The values on the y-axis record the cumulative increases in real disposable income (households and non-profit institutions serving households) in euro per capita in the 5-year period 2020-2024 relative to 2019. For Malta, the disposable income only includes data until 2023.

Third, the governments’ initiatives have helped to make the financial sector more stable and resilient. Particularly, the recapitalisation of banks and the strengthening of the regulatory framework after the financial crisis increased the confidence of banks’ creditors. Banks have substantially reduced the non-performing loans on their balance sheets, which were at historic highs during the debt crisis. This reflects improvements in banking supervision, banks’ efforts to clean up their balance sheets and the shift of risky assets to non-banks. That has strengthened the capital position of the financial sector in the four countries. And it made them more resilient despite the adverse shocks of the last years and the monetary policy tightening.[5]

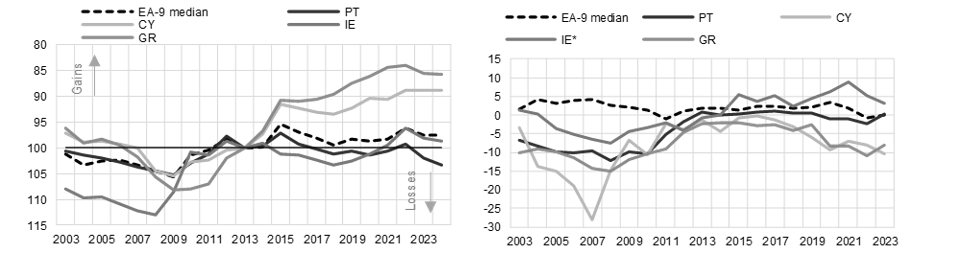

And fourth, external imbalances have been reduced. To appreciate the significance of this turn-around let’s recall the situation before and during the crisis. All four countries had lost price and cost competitiveness (Chart 3 left) and ran large current account deficits, in particular Greece and Cyprus (Chart 3 right). Creditors’ increasingly worried about the four countries’ external financing needs and started to withdraw funding. In response, Ireland improved its competitiveness the quickest among the four thanks to its flexible economic structures and a rapid adjustment of prices and wages. Also, in Cyprus and Greece competitiveness gains have exceeded those in most other euro countries since 2009. In Portugal, though, gains have been more modest and less sustainable. Current account balances also have improved significantly and are now positive in Ireland and Portugal. In Greece and Cyprus, however, they have deteriorated again considerably in recent years, increasing the vulnerability of these economies to an outflow of private capital (Chart 3 right).

Chart 3

Left: Harmonised competitiveness indicator (HCI) GDP deflatedRight: Current account balance

Sources: Eurostat, ECB, Central Statistics Office Ireland, Central Bank of Cyprus, and author’s calculations.

Notes: Left: The HCI index has been inverted, positive (negative) values of HCIs denote a gains (losses) in price and cost competitiveness. The harmonised competitiveness indicators (HCIs) provide an overview of the price and cost competitiveness of each euro area country relative to a group of principal competitors in international markets (rest of EA-20 countries and EER-18 group of non-euro area trading partners). The HCIs GDP deflated can be affected in some countries by the activities of MNEs (IE) or special purpose vehicles (CY). For details on the construction of HCIs see this website: https://www.ecb.europa.eu/stats/balance_of_payments_and_external/hci/html/index.en.html. The 2024 year covers data of the first two quarters only.

Right: For IE* the GNI* and the modified current account balance are used since GDP and non-modified current account balance are distorted by specific transactions of multinational enterprises, which are in part associated with tax optimisation strategies. For CY from 2012 onwards a current account series that excludes the special purpose entities is used.

The economic situation of Greece, Ireland, Portugal and Cyprus has substantially improved over the last decade. Policy measures introduced during the crisis and its aftermath helped to reduce imbalances and led to more growth and steeper declines in public debt compared to most other euro area countries.[6]

Nevertheless, policy makers in the four countries and beyond face large challenges. In particular, public debt is still elevated, external liabilities remain high and productivity growth is low. These weaknesses differ across countries and they may worsen amid new geopolitical challenges, ageing populations, and climate change. Thus, substantial structural policy efforts are still needed to further spur potential growth, safeguard debt sustainability and build economic resilience.[7] As a matter of fact that also holds for many of the other euro area countries, in particular for some of the largest ones.

The views expressed in each blog entry are those of the authors and do not necessarily represent the views of the European Central Bank and the Eurosystem.

Check out The ECB Blog and subscribe for future posts.

For topics relating to banking supervision, why not have a look at The Supervision Blog?

“The European Central Bank is the prime component of the Eurosystem and the European System of Central Banks as well as one of seven institutions of the European Union. It is one of the world’s most important central banks.”

Please visit the firm link to site